Newsletter

About Us |

March 2016Feature Articles

Tax Tips

QuickBooks Tips | Enter your email below to subscribe to our monthly newsletter.

|

Six Overlooked Tax Breaks for Individuals

Confused about which credits and deductions you can claim on your 2015 tax return? You're not alone. Here are six tax breaks that you won't want to overlook.

1. State Sales and Income Taxes

Thanks to last-minute tax extender legislation passed in December, taxpayers filing their 2015 returns can still deduct either state income tax paid or state sales tax paid, whichever is greater.

Here's how it works. If you bought a big-ticket item like a car or boat in 2015, it might be more advantageous to deduct the sales tax, but don't forget to figure any state income taxes withheld from your paycheck just in case. If you're self-employed, you can include the state income paid from your estimated payments. In addition, if you owed taxes when filing your 2014 tax return in 2015, you can include the amount when you itemize your state taxes this year on your 2015 return.

2. Child and Dependent Care Tax Credit

Most parents realize that there is a tax credit for daycare when their child is young, but they might not realize that once a child starts school, the same credit can be used for before and after school care, as well as day camps during school vacations. This child and dependent care tax credit can also be taken by anyone who pays a home health aide to care for a spouse or other dependent--such as an elderly parent--who is physically or mentally unable to care for him or herself. The credit is worth a maximum of $1,050 or 35 percent of $3,000 of eligible expenses per dependent.

3. Job Search Expenses

Job search expenses are 100 percent deductible, whether you are gainfully employed or not currently working--as long as you are looking for a position in your current profession. Expenses include fees paid to join professional organizations, as well as employment placement agencies that you used during your job search. Travel to interviews is also deductible (as long as it was not paid by your prospective employer) as is paper, envelopes, and costs associated with resumes or portfolios. The catch is that you can only deduct expenses greater than two percent of your adjusted gross income (AGI). Also, you cannot deduct job search expenses if you are looking for a job for the first time.

4. Student Loan Interest Paid by Parents

Typically, a taxpayer is only able to deduct interest on mortgage and student loans if he or she is liable for the debt; however, if a parent pays back their child's student loans that money is treated by the IRS as if the child paid it. As long as the child is not claimed as a dependent, he or she can deduct up to $2,500 in student loan interest paid by the parent. The deduction can be claimed even if the child does not itemize.

5. Medical Expenses

Most people know that medical expenses are deductible as long as they are more than 10 percent of Adjusted Gross Income (AGI) for tax year 2015. What they often don't realize is which medical expenses can be deducted, such as medical miles (23 cents per mile) driven to and from appointments and travel (airline fares or hotel rooms) for out of town medical treatment.

Other deductible medical expenses that taxpayers might not be aware of include health insurance premiums, prescription drugs, co-pays, and dental premiums and treatment. Long-term care insurance (deductible dollar amounts vary depending on age) is also deductible, as are prescription glasses and contacts, counseling, therapy, hearing aids and batteries, dentures, oxygen, walkers, and wheelchairs.

If you're self-employed, you may be able to deduct medical, dental, or long-term care insurance. Even better, you can deduct 100 percent of the premium. In addition, if you pay health insurance premiums for an adult child under age 27, you may be able to deduct those premiums as well.

6. Bad Debt

If you've ever loaned money to a friend, but were never repaid, you may qualify for a non-business bad debt tax deduction of up to $3,000 per year. To qualify, however, the debt must be totally worthless in that there is no reasonable expectation of payment.

Non-business bad debt is deducted as a short-term capital loss, subject to the capital loss limitations. You may take the deduction only in the year the debt becomes worthless. You do not have to wait until a debt is due to determine whether it is worthless. Any amount you are not able to deduct can be carried forward to reduce future tax liability.

Are you getting all of the tax credits and deductions that you are entitled to?

Maybe you are...but maybe you're not. Why take a chance? Call the office today and make sure you get all of the tax breaks you deserve.

Who Should File a 2015 Tax Return?

Most people file a tax return because they have to, but even if you don't, there are times when you should because you might be eligible for a tax refund and not know it. This year, there are a few new rules for taxpayers who must file. The six tax tips below should help you determine whether you're one of them.

1. General Filing Rules. Whether you need to file a tax return this year depends on a few factors. In most cases, the amount of your income, your filing status, and your age determine if you must file a tax return. For example, if you're single and 28 years old you must file if your income, was at least $10,300. Other rules may apply if you're self-employed or if you're a dependent of another person. There are also other cases when you must file. If you have any questions, don't hesitate to call.

2. Premium Tax Credit. If you bought health insurance through the Health Insurance Marketplace in 2015, you might be eligible for the Premium Tax Credit; however, you will need to file a return to claim the credit.

If you purchased coverage from the Marketplace in 2015 and chose to have advance payments of the premium tax credit sent directly to your insurer during the year, you must file a federal tax return. You will reconcile any advance payments with the allowable premium tax credit.

You should have received Form 1095-A, Health Insurance Marketplace Statement, in February. The new form has information that helps you file your tax return and reconcile any advance payments with the allowable Premium Tax Credit.

3. Tax Withheld or Paid. Did your employer withhold federal income tax from your pay? Did you make estimated tax payments? Did you overpay last year and have it applied to this year's tax? If you answered "yes" to any of these questions, you could be due a refund. But you have to file a tax return to get it.

4. Earned Income Tax Credit. Did you work and earn less than $53,267 last year? You could receive EITC as a tax refund if you qualify with or without a qualifying child. You may be eligible for up to $6,242. If you qualify, file a tax return to claim it.

5. Additional Child Tax Credit. Do you have at least one child that qualifies for the Child Tax Credit? If you don't get the full credit amount, you may qualify for the Additional Child Tax Credit.

6. American Opportunity Credit. The AOTC (up to $2,500 per eligible student) is available for four years of post-secondary education. You or your dependent must have been a student enrolled at least half-time for at least one academic period. Even if you don't owe any taxes, you still may qualify; however, you must complete Form 8863, Education Credits, and file a return to claim the credit.

Which Tax Form is Right for You?

You can generally use the 1040EZ if:

- Your taxable income is below $100,000;

- Your filing status is single or married filing jointly;

- You don't claim dependents; and

- Your interest income is $1,500 or less.

Note: You can't use Form 1040EZ to claim the new Premium Tax Credit. You also can't use this form if you received advance payments of this credit in 2015.

The 1040A may be best for you if:

- Your taxable income is below $100,000;

- You have capital gain distributions;

- You claim certain tax credits; and

- You claim adjustments to income for IRA contributions and student loan interest.

You must use the 1040 if:

- Your taxable income is $100,000 or more;

- You claim itemized deductions;

- You report self-employment income; or

- You report income from sale of a property.

Questions?

Help is just a phone call away. Call or make an appointment now and get the answers you need today.

IRS Dirty Dozen Tax Scams for 2016

Compiled annually by the IRS, the "Dirty Dozen" is a list of common scams taxpayers may encounter in the coming months. While many of these scams peak during the tax filing season, they may be encountered at any time during the year. Here is this year's list:

1. Identity Theft

Tax-related identity theft occurs when someone uses your stolen Social Security number to file a tax return claiming a fraudulent refund. Taxpayers should use caution when viewing e-mails, receiving telephone calls or getting advice on tax issues because scams can take on many sophisticated forms, according to IRS Commissioner John Koskinen. Taxpayers should secure personal information by protecting their computers and only giving out Social Security numbers when absolutely necessary.

2. Phone Scams

Aggressive and threatening phone calls by criminals impersonating IRS agents remain a major threat to taxpayers. In recent weeks, the agency has seen a surge of these phone scams as scam artists threaten police arrest, deportation, license revocation and other things.

Scammers make unsolicited calls claiming to be IRS officials. They demand that the victim pay a bogus tax bill. They con the victim into sending cash, usually through a prepaid debit card or wire transfer. They may also leave "urgent" callback requests through phone "robocalls," or via a phishing email.

Many phone scams use threats to intimidate and bully a victim into paying. They may even threaten to arrest, deport or revoke the license of their victim if they don't get the money.

Scammers often alter caller ID numbers to make it look like the IRS or another agency is calling. The callers use IRS titles and fake badge numbers to appear legitimate. They may use the victim's name, address and other personal information to make the call sound official.

3. Phishing

Phishing schemes using fake emails or websites are used by criminals to try to steal personal information. Typically, criminals pose as a person or organization you trust and/or recognize. They may hack an email account and send mass emails under another person's name, or pose as a bank, credit card company, tax software provider or government agency. These criminals go to great lengths to create websites that appear legitimate but contain phony log-in pages, hoping that victims will take the bait so they can steal the victim's money, passwords, Social Security number and identity.

Scam emails and websites also can infect your computer with malware without you even knowing it. The malware can give the criminal access to your device, enabling them to access all your sensitive files or track your keyboard strokes, exposing login information.

4. Tax Return Preparer Fraud

About 60 percent of taxpayers use tax professionals to prepare their returns. The vast majority of tax professionals provide honest, high-quality service, but there are some dishonest preparers who set up shop each filing season. Well-intentioned taxpayers can be misled by preparers who don't understand taxes or who mislead people into taking credits or deductions they aren't entitled to in order to increase their fee.

Illegal scams can lead to significant penalties and interest and possible criminal prosecution. IRS Criminal Investigation works closely with the Department of Justice (DOJ) to shutdown scams and prosecute the criminals behind them.

5. Hiding Money or Income Offshore

Through the years, offshore accounts have been used to lure taxpayers into scams and schemes. Numerous individuals have been identified as evading U.S. taxes by hiding income in offshore banks, brokerage accounts or nominee entities and then using debit cards, credit cards or wire transfers to access the funds. Others have employed foreign trusts, employee-leasing schemes, private annuities or insurance plans for the same purpose.

While there are legitimate reasons for maintaining financial accounts abroad, there are reporting requirements that need to be fulfilled. U.S. taxpayers who maintain such accounts and who do not comply with reporting requirements are breaking the law and risk significant penalties and fines, as well as the possibility of criminal prosecution.

6. Inflated Refund

Taxpayers should be on the lookout for unscrupulous tax return preparers pushing inflated tax refund claims. Scam artists routinely pose as tax preparers during tax time, luring victims in by promising large federal tax refunds or refunds that people never dreamed they were due in the first place. They might, for example, promise inflated refunds based on fictitious Social Security benefits and false claims for education credits, the Earned Income Tax Credit (EITC), or the American Opportunity Tax Credit, among others.

Scammers use flyers, advertisements, phony store fronts and even word of mouth to throw out a wide net for victims. They may even spread the word through community groups or churches where trust is high. Scammers frequently prey on people such as the elderly or non-English speakers, who may or may not have a filing requirement.

Because taxpayers are legally responsible for what is on their returns (even if it was prepared by someone else), those who buy into such schemes can end up being penalized for filing false claims or receiving fraudulent refunds.

7. Fake Charities

Taxpayers should be aware that phony charities use names or websites that sound or look like those of respected, legitimate organizations. For instance, following major disasters, it's common for scam artists to impersonate charities to get money or private information from well-intentioned taxpayers. Scam artists use a variety of tactics including contacting people by telephone or email to solicit money or financial information. They may even directly contact disaster victims and claim to be working for or on behalf of the IRS to help the victims file casualty loss claims and get tax refunds. They may also attempt to get personal financial information or Social Security numbers that can be used to steal the victims' identities or financial resources.

8. Falsely Padding Deductions

The vast majority of taxpayers file honest and accurate tax returns on time every year. However, each year some taxpayers fail to resist the temptation of fudging their information. That's why falsely claiming deductions, expenses or credits on tax returns is on the "Dirty Dozen" tax scams list for the 2016 filing season. The IRS warns taxpayers that they should think twice before overstating deductions such as charitable contributions, padding their claimed business expenses or including credits that they are not entitled to receive. Avoid the temptation of falsely inflating deductions or expenses on your return to underpay what you owe and possibly receive larger refunds.

9. Excessive Claims for Business Credits

Improper claims for business credits such as the fuel tax and the research credit are also on the IRS "Dirty Dozen" list this year. The fuel tax credit is generally limited to off-highway business use or use in farming. Consequently, the credit is not available to most taxpayers. Still, the IRS routinely finds unscrupulous preparers who have enticed sizable groups of taxpayers to erroneously claim the credit to inflate their refunds. Fraud involving the fuel tax credit is considered a frivolous tax claim and can result in a penalty of $5,000.

The research credit is an important feature in the tax code to foster research and experimentation by the private sector; however, the IRS does see a significant amount of misuse of the research credit each year. Improper claims for the research credit generally involve failures to participate in or substantiate qualified research activities and/or satisfy the requirements related to qualified research expenses.

10. Falsifying Income

This scam involves inflating or including income on a tax return that was never earned, either as wages or as self-employment income, usually in order to maximize refundable credits. Just like falsely claiming an expense or deduction you did not pay, claiming income you did not earn in order to secure larger refundable credits could have serious repercussions. Well-intentioned taxpayers can be misled by tax preparers who don't understand taxes or who mislead people into taking credits or deductions they aren't entitled to in order to increase their fee.

Remember: Taxpayers are legally responsible for what's on their tax return even if it is prepared by someone else. Make sure the preparer you hire is ethical and up to the task.

11. Abusive Tax Shelters

Phony tax shelters and structures to avoid paying taxes continues to be a problem and taxpayers should steer clear of these types of schemes as they can end up costing taxpayers more in back taxes, penalties, and interest than they saved in the first place.

Abusive tax schemes have evolved from simple structuring of abusive domestic and foreign trust arrangements into sophisticated strategies that take advantage of the financial secrecy laws of some foreign jurisdictions and the availability of credit/debit cards issued from offshore financial institutions. For example, multiple flow-through entities are commonly used as part of a taxpayer's scheme to evade taxes. These schemes may use Limited Liability Companies (LLCs), Limited Liability Partnerships (LLPs), International Business Companies (IBCs), foreign financial accounts, offshore credit/debit cards and other similar instruments. They are designed to conceal the true nature and ownership of the taxable income and/or assets.

Trusts also commonly show up in abusive tax structures. They are highlighted here because unscrupulous promoters continue to urge taxpayers to transfer large amounts of assets into trusts. These assets include not only cash and investments but also successful on-going businesses. There are legitimate uses of trusts in tax and estate planning, but the IRS commonly sees highly questionable transactions. These transactions promise reduced taxable income, inflated deductions for personal expenses, reduced (even to zero) self-employment taxes, and reduced estate or gift transfer taxes. These transactions commonly arise when taxpayers are transferring wealth from one generation to another.

Another abuse involving a legitimate tax structure involves certain small or "micro" captive insurance companies. In the abusive structure, unscrupulous promoters, accountants, or wealth planners persuade the owners of closely held entities to participate in these schemes. The promoters assist the owners to create captive insurance companies onshore or offshore and cause the creation and sale of the captive "insurance" policies to the closely held entities. The promoters manage the entities' captive insurance companies for substantial fees, assisting taxpayers unsophisticated in insurance, to continue the charade from year to year.

12. Frivolous Tax Arguments

Taxpayers are also warned against using frivolous tax arguments to avoid paying their taxes. Examples include contentions that taxpayers can refuse to pay taxes on religious or moral grounds by invoking the First Amendment or that the only "employees" subject to federal income tax are employees of the federal government; and that only foreign-source income is taxable.

Promoters of frivolous schemes encourage taxpayers to make unreasonable and outlandish claims to avoid paying the taxes they owe. These arguments are wrong and have been thrown out of court. While taxpayers have the right to contest their tax liabilities in court, no one has the right to disobey the law or disregard their responsibility to pay taxes. The penalty for filing a frivolous tax return is $5,000.

If you think you've been a victim of a tax scam, don't hesitate to call.

The Individual Shared Responsibility Provision

The individual shared responsibility provision requires that you and each member of your family have qualifying health insurance, a health coverage exemption, or make a payment for any months without coverage or an exemption when you file. If you, your spouse and dependents had health insurance coverage all year, you will indicate this by simply checking a box on your tax return.

In most cases, the shared responsibility payment reduces your refund. If you are not claiming a refund, the payment will increase the amount you owe on your tax return. Here are some basic facts about the individual shared responsibility provision.

What is the individual shared responsibility provision?

The individual shared responsibility provision calls for each individual to have qualifying healthcare coverage--known as minimum essential coverage--for each month, qualify for an exemption, or make a payment when filing his or her federal income tax return.

Who is subject to the individual shared responsibility provision?

The provision applies to individuals of all ages, including children. The adult or married couple who can claim a child or another individual as a dependent for federal income tax purposes is responsible for making the shared responsibility payment if the dependent does not have coverage or an exemption.

How do I get a health coverage exemption?

You can claim most exemptions when you file your tax return. There are certain exemptions that you can obtain only from the Marketplace in advance. You can obtain some exemptions from the Marketplace or by claiming them on your tax return. You will claim or report coverage exemptions on Form 8965, Health Coverage Exemptions, and attach it to Form 1040, Form 1040A, or Form 1040EZ. You can file any of these forms electronically. For any month that you or your dependents do not have coverage or qualify for an exemption, you will have to make a shared responsibility payment

What do I need to do if I am required to make a payment with my tax return?

If you have to make an individual shared responsibility payment, you will need to use the worksheets found in the instructions to Form 8965, Health Coverage Exemptions, to figure the shared responsibility payment amount due. You only make a payment for the months you did not have coverage or qualify for a coverage exemption. If you need assistance, please call.

What happens if I owe an individual shared responsibility payment, but I cannot afford to make the payment when filing my tax return?

The law prohibits the IRS from using liens or levies to collect any individual shared responsibility payment and they routinely work with taxpayers who owe amounts they cannot afford to pay. However, if you owe a shared responsibility payment, the IRS may offset that liability against any tax refund that may be due to you.

Please call the office if you would like more information about the individual shared responsibility provision.

It's Not Too Late to Make a 2015 IRA Contribution

If you haven't contributed funds to an Individual Retirement Arrangement (IRA) for tax year 2015, or if you've put in less than the maximum allowed, you still have time to do so. You can contribute to either a traditional or Roth IRA until the April 18th due date, not including extensions.

Be sure to tell the IRA trustee that the contribution is for 2015. Otherwise, the trustee may report the contribution as being for 2016 when they get your funds.

Generally, you can contribute up to $5,500 of your earnings for tax year 2015 (up to $6,500 if you are age 50 or older in 2015). You can fund a traditional IRA, a Roth IRA (if you qualify), or both, but your total contributions cannot be more than these amounts.

Traditional IRA: You may be able to take a tax deduction for the contributions to a traditional IRA, depending on your income and whether you or your spouse, if filing jointly, are covered by an employer's pension plan.

Roth IRA: You cannot deduct Roth IRA contributions, but the earnings on a Roth IRA may be tax-free if you meet the conditions for a qualified distribution.

Each year, the IRS announces the cost of living adjustments and limitation for retirement savings plans.

Saving for retirement should be part of everyone's financial plan and it's important to review your retirement goals every year in order to maximize savings. If you need help with your retirement plans, give the office a call.

Choosing the Correct Filing Status

It's important to use the right filing status when you file your tax return because the filing status you choose can affect the amount of tax you owe for the year. It may even determine if you must file a tax return. Keep in mind that your marital status on Dec. 31 is your status for the whole year. Sometimes more than one filing status may apply to you. If that happens, choose the one that allows you to pay the least amount of tax.

The easiest and most accurate way to file your tax return is to consult a tax professional who is able to choose the right filing status based on your circumstances. Here's a list of the five filing statuses:

1. Single. This status normally applies if you aren't married. It applies if you are divorced or legally separated under state law.

2. Married Filing Jointly. If you're married, you and your spouse can file a joint tax return. If your spouse died in 2015, you can often file a joint return for that year.

3. Married Filing Separately. A married couple can choose to file two separate tax returns. This may benefit you if it results in less tax owed than if you file a joint tax return. You may want to prepare your taxes both ways before you choose. You can also use it if you want to be responsible only for your own tax.

4. Head of Household. In most cases, this status applies if you are not married, but there are some special rules. For example, you must have paid more than half the cost of keeping up a home for yourself and a qualifying person. Don't choose this status by mistake. Be sure to check all the rules.

5. Qualifying Widow(er) with Dependent Child. This status may apply to you if your spouse died during 2013 or 2014 and you have a dependent child. Other conditions also apply.

Don't hesitate to call if you have any questions about filing your tax return this year.

Exemptions and Dependents: Top Ten Tax Facts

Most people can claim an exemption on their tax return. It can lower your taxable income, which in most cases, that reduces the amount of tax you owe for the year. Here are eight tax facts about exemptions to help you file your tax return.

1. Exemptions Cut Income. There are two types of exemptions. The first type is a personal exemption. The second type is an exemption for a dependent. You can usually deduct $4,000 for each exemption you claim on your 2015 tax return.

2. Personal Exemptions. You can usually claim an exemption for yourself. If you're married and file a joint return, you can claim one for your spouse, too. If you file a separate return, you can claim an exemption for your spouse only if your spouse:

- Had no gross income,

- Is not filing a tax return, and

- Was not the dependent of another taxpayer.

3. Exemptions for Dependents. You can usually claim an exemption for each of your dependents. A dependent is either your child or a relative who meets a set of tests. You can't claim your spouse as a dependent. You must list the Social Security number of each dependent you claim on your tax return. To learn more about these rules, please call the office.

4. Report Health Care Coverage. The health care law requires you to report certain health insurance information for you and your family. The individual shared responsibility provision requires you and each member of your family to either:

- Have qualifying health insurance, called minimum essential coverage, or

- Have an exemption from this coverage requirement, or

- Make a shared responsibility payment when you file your 2015 tax return.

Please call if you'd like more information about these rules.

5. Some People Don't Qualify. You normally may not claim married persons as dependents if they file a joint return with their spouse. There are some exceptions to this rule.

6. Dependents May Have to File. A person who you can claim as your dependent may have to file their own tax return. This depends on certain factors, like total income, whether they are married and if they owe certain taxes.

7. No Exemption on Dependent's Return. If you can claim a person as a dependent, that person can't claim a personal exemption on his or her own tax return. This is true even if you don't actually claim that person on your tax return. This rule applies because you can claim that person as your dependent.

8. Exemption Phase-Out. The $4,000 per exemption is subject to income limits. This rule may reduce or eliminate the amount you can claim based on the amount of your income.

Questions? Help is just a phone call away!

What QuickBooks' Calendar Can Do for You

These days, some of us find ourselves updating multiple calendars. There's the Outlook calendar or other web-based solution for scheduling and task management. Or, maybe a smartphone app to track a "to-do" on the road with a paper calendar as backup.

But where do you keep track of your everyday financial tasks? Including these in your scheduling calendars and/or task lists will make for very crowded screens, not to mention how inconvenient it can be to keep switching between applications.

Consider adding one more tracking tool: the QuickBooks calendar. This graphical screen isn't designed for data entry (except for the to-do list); rather, it's designed to give you a quick overview of your financial activity, both historically and in the future.

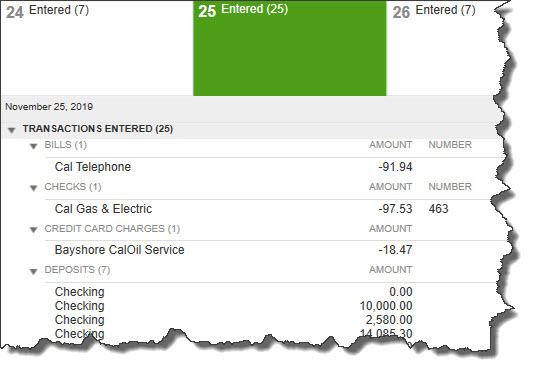

Figure 1: The QuickBooks calendar consists of two parts. The graphical calendar itself displays one of three types of entries: Entered, Due, or To Do. The number in parentheses refers to the number of each type that occurred or will occur that day. Details of each entry appear below; double-clicking on one opens the original form.

Calendar Setup

Before you start using the QuickBooks calendar, you should designate your display and content options. Open the Edit menu and select Preferences | Calendar. Make sure that the My Preferences tab is active.

Click on the arrows to the right of every field to open the menu that displays your choices. The first of these are:

- Calendar view. Daily? Weekly? Monthly? Or do you want QuickBooks to remember the last view that was open?

- Weekly view. Should the calendar only display the primary workdays or all seven?

- Show. What items would you like to have displayed on the calendar? It defaults to All Transactions, but you can filter it by transaction type.

You can also specify whether you want past due and upcoming entries to be included, and for how many days.

Tracking your "To-Do"

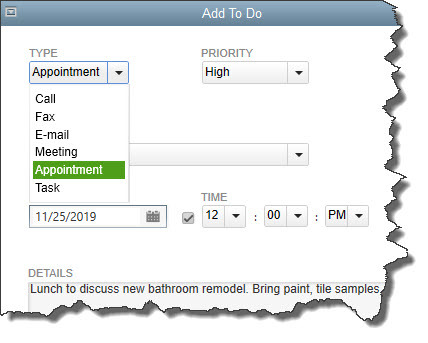

Figure 2: You can create to-do items and have them appear on the QuickBooks calendar.

The QuickBooks calendar also offers tools for creating a to-do list of several types (call, fax, email, meeting, appointment, or task). These will appear on the calendar unless you filter them out.

Tip: The link that opens the to-do window is somewhat hard to find, but is located in the lower right corner of the graphical calendar.

Click on Add To Do to get started. The window pictured above opens. Click the arrow to the right of the field under TYPE and select the type of to-do that you want to define. You can also select a PRIORITY level if you'd like.

Below those two fields is a small box to the left of WITH. If you want to connect that activity to a customer, vendor, or employee, click in the box and select the type. Then click the arrow next to the field below it and choose the correct individual or company.

You aren't required to create this link; you can simply designate your to-do type and enter a DATE, TIME, and DETAILS. The activity will still appear on your QuickBooks calendar. But if you do associate it with a specific entity, like a customer, it will appear in that customer's record when you click on the To Do tab.

A Word About Reminders

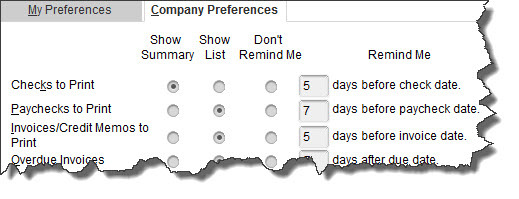

Figure 3: You can get advance notice of scheduled financial activities by setting up Reminders. Go to Edit | Preferences | Reminders | Company Preferences.

The QuickBooks calendar is not really a reminder tool. You'll need to use QuickBooks' Reminders to get help with advance notice of due dates.

But the calendar will display the actual due dates for transactions. If you've entered a bill that's due on February 28, for example, the word Due will appear on that date in the graphical calendar; the number of transactions due will appear in parentheses after it. All entries for that day appear in a list below. To see the original form, you'd double-click on the one you want to see.

Using Reminders in conjunction with the QuickBooks calendar can help you stay current with sales and purchases - if you have you due dates established in a way that will be good for your cash flow. Call the office if you need help scheduling incoming and outgoing payments in a way that will work to your advantage.

Tax Due Dates for March 2016

March 10

Employees who work for tips - If you received $20 or more in tips during February, report them to your employer. You can use Form 4070.

March 15

Employers - Nonpayroll withholding. If the monthly deposit rule applies, deposit the tax for payments in February.

Employers - Social Security, Medicare, and withheld income tax. If the monthly deposit rule applies, deposit the tax for payments in February.

Corporations - File a 2015 calendar year income tax return (Form 1120) and pay any tax due. If you want an automatic 6-month extension of time to file the return, file Form 7004 and deposit what you estimate you owe.

S Corporations - File a 2015 calendar year income tax return (Form 1120S) and pay any tax due. Provide each shareholder with a copy of Schedule K-1 (Form 1120S), Shareholder's Share of Income, Credits, Deductions, etc., or a substitute Schedule K-1. If you want an automatic 6-month extension of time to file the return, file Form 7004 and deposit what you estimate you owe.

Electing large partnerships - Provide each partner with a copy of Schedule K-1 (Form 1065-B), Partner's Share of Income (Loss) From an Electing Large Partnership. This due date applies even if the partnership requests an extension of time to file the Form 7004.

S Corporation Election - File Form 2553, Election by a Small Business Corporation, to choose to be treated as an S corporation beginning with calendar year 2016. If Form 2553 is filed late, S treatment will begin with calendar year 2017.

March 31

Electronic filing of Forms 1097, 1098, 1099, 3921, 3922, and W-2G - File Forms 1097, 1098, 1099, 3921, 3922, or W-2G with the IRS. This due date applies only. The due date for giving the recipient these forms generally remains February 1.

For information about filing Forms 1097, 1098, 1099, 3921, 3922, or W-2G electronically, see Publication 1220, Specifications for Electronic Filing of Forms 1097, 1098, 1099, 3921, 3922, 5498, and W-2G.

Electronic filing of Forms W-2 - File copies of all the Forms W-2 you issued for 2015. This due date applies only if you electronically file. Otherwise see February 29. The due date for giving the recipient these forms remains February 1.

Copyright © 2016 All materials contained in this document are protected by U.S. and international copyright laws. All other trade names, trademarks, registered trademarks and service marks are the property of their respective owners.

Get In Touch

At Excel Accounting & Tax LLC, we've been serving the accounting needs statewide. If you need help managing any aspect of your home or business's finances, we want to hear from you.

Please call us or fill out this form and let us know how we can be of service. We will happily offer you a FREE initial consultation to determine how we can best serve you.

Thank you for visiting. We look forward to working together!